Cost of Chaos

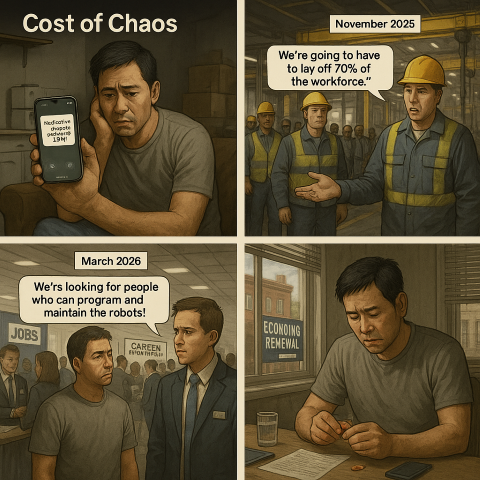

Michael Chen stared at the notification on his phone. His diabetes medication had gone up another 15% this month. He closed the pharmacy app and glanced around the small studio apartment he’d been renting since selling his house. The worn couch that doubled as his bed, the kitchenette with its single burner stove, the piles of cardboard boxes he still hadn’t found the energy to unpack—all of it felt surreal compared to where he’d been just two years ago.

In 2024, Michael had been thriving in Cleveland. At 42, he’d worked as a production manager at an auto parts manufacturing plant that supplied components to several major automotive companies, including some Chinese partnerships. He’d owned a modest three-bedroom house in a good neighborhood, had decent health insurance through his employer, and had been steadily building his 401(k). His daughter had just started college, and Michael had been proud he could help with her tuition.

The trade war changed everything. When the tariffs hit Chinese imports in early 2025, followed by China’s retaliation, Michael’s company was caught in the crossfire. Their Chinese partners pulled out, and export orders collapsed by nearly 80%. The manufacturing sector in Ohio was devastated, with plants closing across the region.

His company held on for six months, trying to pivot to domestic suppliers and customers, but the reshoring boom that politicians had promised never materialized. By November 2025, the plant announced layoffs. Michael, along with 70% of the workforce, lost his job.

“Things will turn around,” his former supervisor had said. “Manufacturing always bounces back.”

But it hadn’t. Not in the Midwest. While tech hubs in California and Texas boomed with AI and semiconductor investments, traditional manufacturing regions like Ohio continued to stagnate. Michael watched as friends and former colleagues struggled to find work in a region where unemployment had climbed to nearly 6%.

At first, he’d been optimistic. With two decades of manufacturing experience and a community college degree, he’d always found work before. But the landscape had changed. Most job postings now required AI-specific skills or experience with automated systems that Michael didn’t have.

He’d attended a job fair in March 2026, where a recruiter for a new robotics facility had been brutally honest: “We’re looking for people who can program and maintain the robots, not operate the machines themselves.”

Meanwhile, his savings dwindled. His unemployment benefits covered less than half of his former salary, and they’d been shortened from nine months to just six due to state budget cuts. The high-deductible health insurance plan he’d found on the exchange cost three times what he’d paid through his employer, and the coverage was worse.

When he developed Type 2 diabetes in late 2025—stress and poor diet, the doctor had said—the medical bills started piling up. He dipped into his 401(k), paying the penalty and watching his retirement dreams fade.

By April 2026, he’d made the hardest decision of his life: selling his house. The market was down 10% from its peak, but he needed the cash. He paid off his credit cards and medical debt, moved into a studio apartment on the edge of town, and tried to regroup.

“Dad, I can drop out for a semester,” his daughter had offered during their weekly video call. “I can work and send money home.”

“Absolutely not,” he’d insisted, forcing a smile. “Your education comes first. I’m fine.”

He wasn’t fine. Last week, the healthcare clinic he relied on had announced it was closing—the fifth rural clinic in the region to shut its doors this year. Now he’d have to drive an hour to the city for his check-ups.

Michael scrolled through job listings on his phone—warehouse associate, security guard, delivery driver—all paying less than 60% of his former salary. He’d applied to dozens of positions, but at 44, competing against younger workers and automated systems, he’d received only two callbacks and no offers.

The news played in the background on his small TV. Commentators discussed the economic “transformation” underway, how AI and automation were driving unprecedented productivity in tech sectors. The stock market had recovered somewhat since the 2025 crash, but the benefits weren’t reaching places like Cleveland.

Michael knew the statistics. Manufacturing jobs in Ohio were down 7% since the trade war began. Opioid deaths had risen 10% in the region. Three people on his former block had lost their homes to foreclosure.

His phone buzzed with a text from his neighbor, an older man who’d lost his job at the same plant.

“Food bank’s got extra this week. Want me to pick you up something?”

Michael stared at the message. Two years ago, he’d been donating to that food bank. Now he was considering whether his pride could withstand becoming a recipient.

His diabetes medication reminder chimed again. He’d been splitting pills to make them last longer—a dangerous practice his doctor had warned against. With the clinic closing and medication costs rising, he wasn’t sure how long he could manage his condition.

Outside his window, a campaign sign for the 2026 midterms promised “Economic Renewal.” Michael had heard those promises before. Meanwhile, the tech executives and hedge fund managers the news kept celebrating seemed to live in a different America altogether—one insulated from tariffs, job losses, and failing safety nets.

He texted his neighbor back: “Thanks. I’ll come with you.”

As he set his phone down, Michael wondered if he’d ever find stable footing in this new economy—one that seemed built for algorithms and automation, but not for people like him caught in the chaos of economic transformation.